With the Dow Jones and S&P 500 at or near record highs, it may seem like the market is firing on all cylinders. While this may be true for most companies, there are some where the outlook might not be so rosy.

The Motley Fool asked three of their analysts what stocks they have sold recently, and why. Here is what they had to say.

1. Eric Volkman: I'll go a bit contrarian here and point the finger at current tech darling Nokia (NOK), which just released Q3 results that made a lot of people happy. I sold shares of the company after its devices and services unit was bought in last year's blockbuster deal with Microsoft (MSFT). And I'm still happy I did, even though the stock price has crept up a few dollars since then.

Related: Warren Buffett Tells You How to Turn $40 Into $10 Million

These days, Nokia is a one-trick pony, with its Networks unit contributing a steep 88% to total revenues. Contrast that with a rival like Alcatel-Lucent (ALU), which at a recent 44% is much better diversified across various segments of the market.

In any corner of tech, concentrating more or less on only one thing -- no matter how well -- leaves a company too vulnerable. This is particularly true in the mobile sphere, which is disruptive and quick to change on even the most sluggish of days. And Alcatel-Lucent is hedged against this somewhat with a balanced product mix; Nokia is not.

Lastly, I think this current iteration of Nokia still needs to prove it can thrive. Before Q3 its bottom line saw three straight quarters of declines. One reversal does not a trend make.

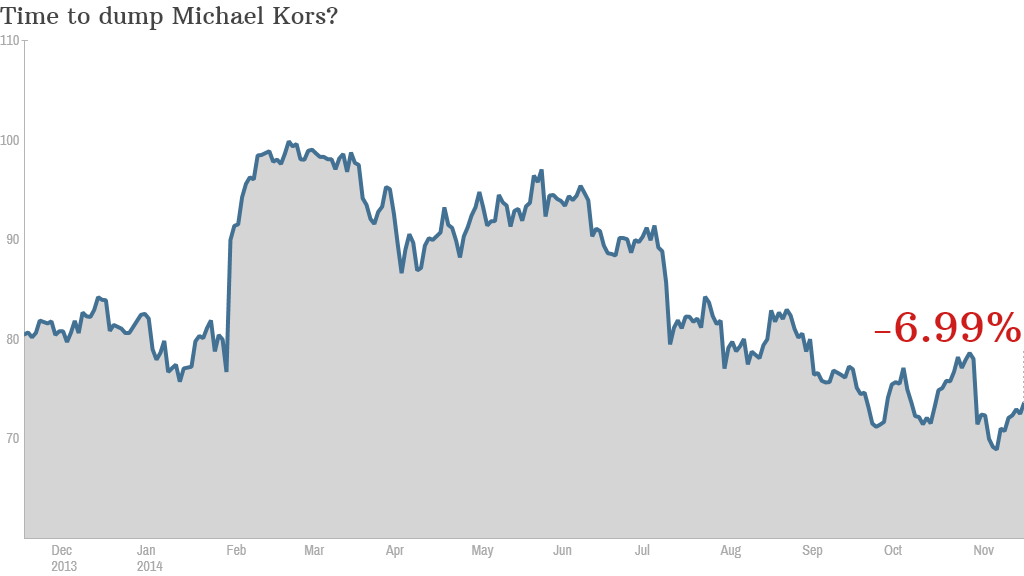

2. Leo Sun: I recently sold my shares of Michael Kors (KORS) because it looked destined to repeat the mistakes that Coach (COH) made -- over-expanding, cutting prices, and undermining its own luxury appeal. Last quarter, Kors' comparables respectively rose 10.8%, 41.1%, and 52.9% in North America, Europe, and Japan. However, analysts had expected North American comparables to rise 15%.

Meanwhile, operating margins at Michael Kors' retail, wholesale, and licensing segments all declined from the prior year quarter. Although the declines were minor, the company's 2015 outlook confirmed an upcoming slowdown. Kors projected third quarter earnings between $1.31 and $1.34 per share on revenue between $1.27 billion and $1.3 billion, assuming a "low double digit compare store sales increase." That barely met the consensus estimate of $1.34 per share on revenue of $1.3 billion. It also expects comparables growth in the "mid-teens" -- quite a slowdown from the 40.1% and 26.2% comparables growth it reported in fiscal 2013 and 2014.

Related: How to Pay for College: The Affordable Option Many Americans Ignore

If Kors' slowdown continues, it will be forced to slash prices as sales growth stalls. When that happens, minor margin declines will become big ones, and profits will plunge.

3. Matt Frankel: I have been a Prospect Capital Corporation (PSEC) shareholder for some time now, but lately I have started to scale back my position a little bit. There are a couple of reasons I'm starting to get a little skeptical of Prospect.

First is the company's strange dividend announcement. Prospect usually declares three months' worth of dividends at a time, and well in advance. For example, in May, the company declared its dividend payments through the end of the year.

Related: Social Security: 5 Facts You Must Know

However, when the company announced its most recent earnings in September, no such announcement was made. After investors were clearly concerned about this, the company declared its January 2015 dividend to calm everyone down, but it's not working. Now, in the company's most recent earnings release, it said it doesn't intend to announce any further distributions until February.

And, Prospect has been selling shares below net asset value according to a proxy filing from September, and asked shareholders for approval to continue to do so. In the past, Prospect has said sales below net asset value were for extreme situations, so this is definitely troubling.

Having said all of that, I still believe in Prospect as a business, and think that shares represent a decent risk/reward at the current price. Still, my perceived risk has risen, so I felt the need to reduce my exposure.

This article originally appeared in The Motley Fool and is republished here with permission.